Intro to Top 10 Things to Know About the VA Loan before your Panhandle PCS

Hey, it’s Charlie Cameron from the Military Home Team at exp Realty. I’m here with my friend Albert Sousa, the owner of Mortgage Apex. We’re here to talk to you today about 10 things you should know about the VA loan for your military PCS to the Florida Panhandle – whether that’s to Eglin Air Force Base, Hurlburt Field, Naval Air Station Pensacola, Whiting Field, Tyndall Air Force Base, Duke Field, EOD School, 7th Special Forces Group, or elsewhere! The VA mortgage loan is one of the best – perhaps THE best – loan products available on the market, and the VA loan benefit is only available to military veterans, active-duty service members, and surviving spouses.

1 – The VA Loan is Zero Down!

The first VA home loan benefit that most people know is that VA home loans are zero down. You don’t have to put a down payment. So most loan types – whether conventional, FHA, private lenders – you may have to put 20%, 10%, 5% down, but the VA loan can be as low as 0% down. Yeah, it’s an awesome loan product. It’s the best one out there in, in our opinion, as a military member and just in general compared to, to all the other loans out there for the public.

2 – Zero Down Does NOT Mean Zero Cash to Close!

The second thing to know is that even though it’s zero down, it’s not zero cash to close. What I mean by that is you still have to bring closing costs to the table.

I usually tell my clients to estimate about $3,000 for every a hundred thousand dollars of price in this general area in the Florida Panhandle. So as a VA buyer, you do still have to bring some money to the table. For example, if it’s a $300,000 home, I would tell them to expect to bring about $9,000-10,000 to the closing table.

Now that’s not to say we can’t get closing costs paid for. In fact, I’ve had clients and even myself that have closed VA loan homes and gotten a check at the closing table. So it’s totally possible, especially if it’s more of a buyer’s market.

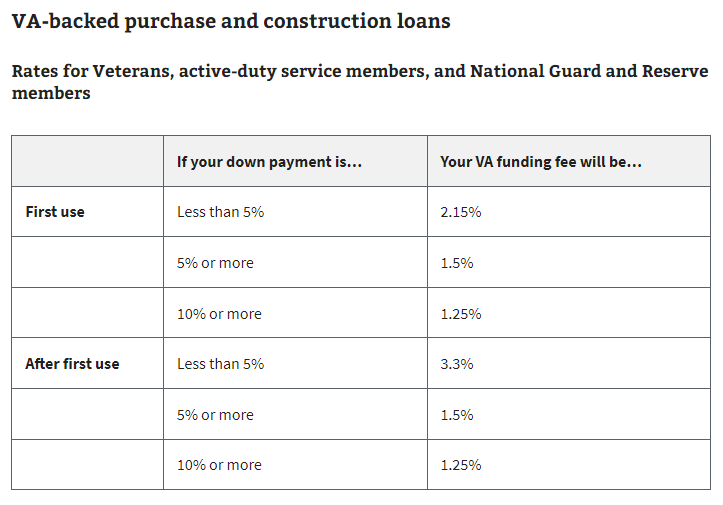

3 – The VA Loan has a Funding Fee that’s Rolled into the Loan

Now, part of the closing costs is a VA funding fee, and that can be a anywhere between 1.25% to 3.3% of your loan amount. But you don’t have to pay for it out of pocket, rather the VA funding fee gets rolled into the loan amount! The VA funding fee essentially replaces private mortgage insurance or PMI – which you typically would see on a conventional loan added to the monthly payment if you had less than 20% down.

Learn more about VA funding fees and the VA loan on the US Department of Veteran Affairs website.

4 – VA Appraisal is also an Inspection & Can Require Repairs

Another benefit of the VA loan. And so the fourth thing you need to know is that the appraisal for the VA loan can come with required repairs. So closing the home can be subject to completing a few repairs. And we see that sometimes on loans. I would say in the past three years it’s probably been about a vast minority of the time we’ve had to have repairs to, to do before closing. Um, but that’s something to keep in mind. You definitely want your, your lender and agent team to be on top of that, to get that appraisal done quickly and make sure we get those addressed. And that’s actually a good thing because the whole thing is the VA loan program is looking out for you. They wanna make sure you’re not buying a house that’s fallen apart. So that’s actually a benefit of the VA loan.

5 – VA Interest Rate Reduction Refinancing Loans (IRRRLs)

Now one of the other huge benefits of the VA loan is being able to do a VA earl. So that is an interest rate reduction loan refinance loan. And so basically it’s the easiest possible loan to lower your interest rate. You don’t have to provide nearly as many documents. Uh, the closing costs are minimal, no appraisal. And so that’s huge. Even if you were to turn it into an investment property in the future, it still gets treated as if it’s a primary. So that is a huge, huge benefit of the VA loan. Definitely something to keep in mind if you’re worried about interest rates and and wanting to get a lower rate later. The VA loan is one of the best opportunities for that.

6 – Yes, You CAN Use the VA Loan More Than Once!

Now, coming in at number six, the things you need to know about the VA loan, you can use it more than once. So even though you’ve used a VA loan in the past, it is okay. We PCS we move around a lot in the miliary. Thankfully Uncle Sam has thought of that and allows us to use the VA loan more than one time. In fact, you can use it over and over and over. To check on your VA loan eligibility, simply check with a VA lender like Albert and the Mortgage Apex team!

7 – Yes, You CAN Have More than One VA Loan at a Time!

And you can actually have more than one at a time. So you can live in your current home, you get orders, you go to a new one, you probably still have more entitlement than you think. And all that means is you basically have limit of how much VA loan you can get. And so oftentimes you can get one, two, have you even seen where people get three VA loans and if you start running low on that entitlement, there are ways for us to free those up through refinances. The best thing to do to check your loan eligibility requirements is to talk to a VA lender!

Yeah, and so that’s a lot of thing military members will do. They’ll purchase a home at one duty station, turn into a rental, move to the next one, and you still have eligibility to use the VA loan again.

8 – The VA Loan has a Lower Interest Rate

And another benefit of the VA loan, is that there are typically lower interest rates available than other loan types like a conventional mortgage. It will still be dependent on factors like credit score, income, debt-to-income ratio, but right now we’re seeing VA loan rates coming in about half a percent lower than their respective conventional loans. So that competitive interest rate means savings for you! That means more buying power.

9 – VA Loan 60 Day Intent to Occupy Clause

Um, number nine, 60 day intend to occupy. So that just means that if you have orders or you’re, you’re gonna move on a specific date, um, lenders are have guidelines that require them to ensure that you’re actually going to move into that home within 60 days of your closing date. So because our timelines to close are at least 30 days, we usually, um, won’t start looking at homes for our clients until we’re close to a, a three to four month window, closer to three months to ensure we don’t violate that rule.

But that means it’s possible for you to have a home ready for you when you move, right? That’s right. And we prefer that for our military members cuz you never know when your household goods are gonna show up. We’ve all been there. Um, there’s a lot of shenanigans and so we, we try and make sure that the home is closed and ready for you with keys in hand when you show up.

10 – Primary Residence Only… But Can Become a Rental Later to Build Wealth!

Now, with that, it does have to be a primary residence for you use your VA loan, but that’s only in the beginning. Once you live in it and live in it for at least a year, you get orders, whatever it is down the road, there’s no stipulations preventing you from turning that home into a income producing rental property.

Bonus: Become a Military Millionaire with the VA Loan!

And here’s a quick secret. You know, after we’ve got through those 10 things to know about the VA loan, most people’s wealth, they’re net worth, the vast majority of it comes from home ownership.

So the VA loan with zero down is one of the best possible products you can use to increase your wealth as active duty service members by purchasing properties and turning a rental, rental properties, homeowners have way more wealth than their respective renters. And so if you want to build wealth, literally you just need to get into the category of homeowner versus renter.

How to Learn More: Work with the Panhandle’s Military First Real Estate Team & Our VA Lenders!

So again, thank you for watching. If you need anything at all, please feel free to reach out to the Military Home. Hit us up on our Facebook community, the Panhandle PCs community on Facebook. And Albert’s team at Mortgage Apex is here to help as well. So just reach out any way you want and we’ll take care of you!